Seyfarth Synopsis: Recently the IRS issued Rev. Proc. 2025-32 and 2025-61, announcing the cost-of-living adjustments to certain welfare and fringe benefit plan limits for 2026 and applicable dollar amounts for the remainder of 2025.

2026 Limits for Certain Health and Fringe Benefits

The Affordable Care Act (ACA) established the Patient-Centered Outcomes Research Institute (“PCORI”), to support research on clinical effectiveness. The PCORI is funded (through the Patient-Centered Outcomes Research Trust Fund) in part by fees paid by certain health insurers and sponsors of self-insured health plans (“PCORI fees”). The PCORI fee is determined by multiplying the average number of covered lives for the plan year times the applicable dollar amount, and is reported and paid annually (by July 31) to the IRS using Form 720 (Instructions to Form 720 are available here). The applicable dollar amount as set by the IRS for plan years ending on or after October 1, 2024 and before October 1, 2025 was $3.47 per covered life.

The IRS has issued Notice 2025-61 announcing the applicable dollar amount that must be used to calculate the fee for plan years that end on or after October 1, 2025, and before October 1, 2026. This 2025-61 PCORI fee is $3.84 per covered life, an increase of $0.37 per covered life from 2025. The PCORI fee for a 2025 calendar plan year, calculated as $3.84 per covered life, is due by July 31, 2026.

For more information on paying the PCORI fee, see our prior posts here and the IRS website here. Also refer to this IRS page for a helpful chart describing the applicability of the PCORI fee to various health arrangements.

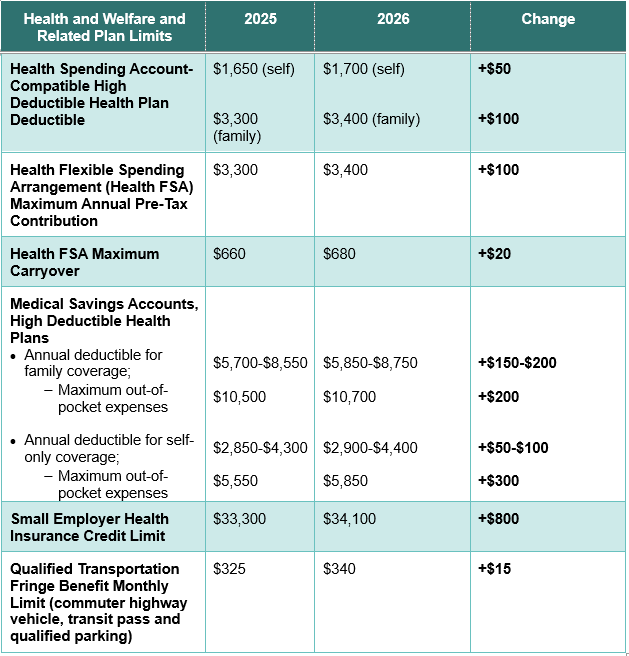

On October 9, 2025, the IRS announced 2026 cost-of-living adjustments to various tax related limits, including the dollar limits for contributions to health flexible spending accounts (Health FSAs) and qualified transportation fringe benefit programs.

The 2026 cost-of-living adjustments (and the changes from 2025) for these plans, from 2025-32 and 2025-61 are summarized in the table below:

Please contact the employee benefits attorney at Seyfarth Shaw LLP with whom you usually work if you have any questions regarding these or other limits on health and welfare and related plans.